Rule one: Know the definitions and then the rest is almost evident.

Return to player (RTP) is the average which a player would win per bet if he were to play many million bets divided by the cost of the bets he placed. “many millions bets” provides an indication that the RTP is defined as the average winning ratio per bet.

Deliberately, I started with the description of the RTP and not with the definition to hint towards a statistical feature of an average, which is based on discrete events, i.e. the various classes or tiers of winnings. For most discrete, random events, the average cannot be realized in a single draw.

Let us take a simple example: The game consists of flipping a fair coin and a bet costs 1 Euro. The payout for heads is EUR 1 and no payout for tails, then the RTP for this game is 50%. But a player can never win 50 cent in a draw. The RTP is only relevant if plays many bets. If he places a 1,000 bets, then he can expect to win 500 Euros.

For more complex games like EuroMillions, Eurojackpot, German 6 out of 49, many more bets are required to get close to the RTP because the chances to win large amounts are very small and small winnings are more frequent. Mathematicians call this an asymmetrical or skewed distribution.

So, who cares about the RTP? To some extent the player cares although there are more relevant statistical key figures for players such as the overall odds to win anything. The regulator who polices the operators on behalf of the players is the one who cares most that the RTP is above a minimal threshold. Most regulators approve lottery style games with RTPs of more than 45%. For casino games like slot machines, the RPT requirement is often 90% or more.

For operators that do not use insurance to cover their liability to payout large winnings there is a simple, straightforward relation between the RTP and the margin:

Margin = 100% – RTP

Typically, this applies to state lottery operators. In contrast, online, secondary lottery companies are unable to pay out very large winnings unless they are covered by an insurance policy to pay out those winnings. In an earlier blog (http://fortanachltd.com/business-models-insurance-vs-messenger/) we described a second model that allows a lottery company to transfer the risk of any winning: The messenger model. Unfortunately, the messenger model can only be applied for official state lottery games – no game innovation possible – and the achievable margin is usually less than 10%.

Let us now explore how the margin for a insurance-based lottery operator has to be calculated. The margin is no longer defined in terms of the RTP. We have to split the winning tiers into two groups:

- Tiers for which the operator transfers the payout of a winner to the insurance. He swaps his liability to payout the winnings him selves against a premium of insuring these winnings. Consequently, for these tiers the average payout does not enter the margin calculation. It is insurance premium for a bet which is relevant.

Obviously, the premium is higher than the average payouts for these tiers. Insurers would not assume the risk of having to pay a large winning and only receiving the long-term average of payouts. From this we conclude that the margin of a state lottery is higher than the margin of a secondary lottery operator. - Tiers for which the operator pays the winners out of his cash reserves. For this group we calculate the normal average payout per bet.

Thus, for secondary lottery operators the margin is:

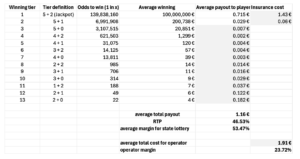

Let us make an example for EuroMillions draw with

- a jackpot of EUR 100m

- ticket price EUR 2.50

- insurance on tier 1 and tier 2 winnings

- insurance cost per tier: 200% of the expected loss to the insurance, i.e. the payout divided by the odds of winning

The higher the jackpot, the lower the operator’s margin as the only variable in the insurance premium calculation is the amount insured. If the jackpot is EUR 30m, then the insurance costs for the jackpot drop to 43 cents and the margin increases to 63.76%.

Note: Most operators will have to switch to the messenger model before their margin decreases to the level of margin offered by the messenger model because they do not have enough insurance capacity to cover very large jackpots. To cover very large jackpots, insurers require a sizable minimum premium which in turn requires the operator to sell a lot of bets. An operator’s volume determines how much insurance limit he can afford.